In recent weeks, Brazil's new fiscal framework and the government's proposals for it have been a topic of discussion. Fiscal convergence has been a long-standing issue, and multiple governments have attempted to address it from two perspectives.

The first perspective is tax simplification, which aims to reduce the number of taxes at the local, regional, and federal levels. Brazil's tax system is considered one of the most inefficient in the world, taking many days to prepare the income tax return and raising the risk of tax evasion. While this focus would improve long-term productivity and GDP, it is considered neutral. The Bolsonaro administration adopted this approach before the COVID-19 pandemic prevented its progress.

The second perspective is increasing tax revenue to finance higher permanent expenditures with fiscal responsibility. However, governments have typically financed expenditures with increased borrowing. Therefore, the market has positively received the current proposal to address this issue.

The current fiscal proposal presented by Finance Minister Fernando Haddad aims to address the second and considers the impact that the tax reform currently in Congress would have. The proposal's main points establish a fiscal anchor that indicates that primary public spending would increase between 0.6% to 2.5% annually in real terms. This increase in spending would be limited to 70% of tax revenue, which would improve primary results and prevent a debt spiral.

The initial perspective on the proposal was negative prior to the announcement, but signs of fiscal responsibility show a more reasonable stance from the government. The market's reaction has been positive, with nominal bond rates at 10 years dropping from 13.75% at the beginning of the month to 12.64% currently, despite the adverse international scenario. The 5-year CDS has also improved from levels higher than 260 basis points at the beginning of the month to 226 basis points currently.

However, some analysts mention that the forecasts presented by the government are optimistic. They point to fiscal deficits of 0.5% for 2023 and beyond, as well as the implicit potential GDP of 1.5% or higher, when most put it around 1.0%. This would require more aggressive revenue-raising measures and/or fiscal cuts for fiscal convergence towards the end of the five-year horizon.

To assess fiscal sustainability, we need to consider various scenarios and examine the most relevant variables. In this regard, the real interest rate and potential economic growth are critical factors. In the short term, we can rely on Bloomberg's median forecast for economic growth, but we need to account for the uncertainties in real interest rates and fiscal deficit projections.

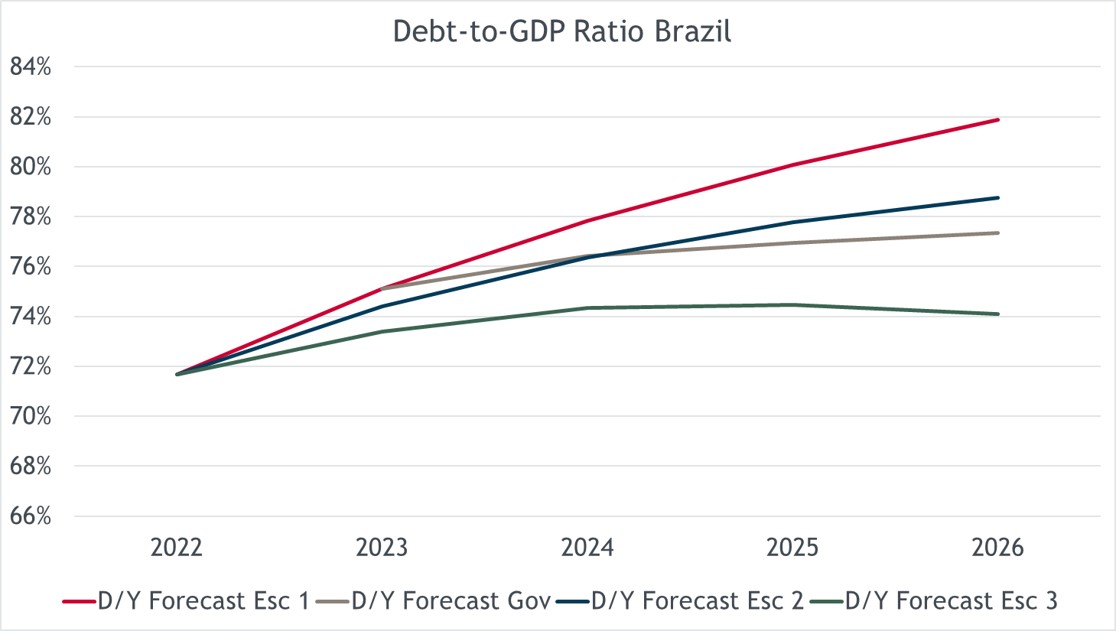

Based on these assumptions, we can envisage three possible scenarios. In the first scenario, if the government implements the proposed spending cuts, but short-term real interest rates remain above 5.0%, the debt-to-GDP ratio would surge from the current 71.9% to 81.9% by 2026. This would be primarily due to the government's lack of ambition in achieving fiscal results.

In the second scenario, assuming a more optimistic interest rate of 4.0% in real terms, the government needs to take aggressive steps to reduce the primary fiscal deficit to 0.0% for 2023 and 2024. It would also need to achieve a primary fiscal surplus of 0.5% and 1.0% for 2025 and 2026, respectively, to reach a debt level of 77.4% of GDP by 2026.

The third scenario involves achieving fiscal convergence by setting extremely ambitious targets. For instance, if the government aims to achieve a fiscal surplus of 0.50% in the early years, and even 2.0% in 2026, it can stabilize the debt at 75% of GDP and achieve a slight decrease in 2026.

The simulated results can be seen in the following graph:

Looking ahead, a slightly better-than-expected fiscal anchor could have a profound impact on the domestic interest rates. This theory has been gaining momentum in the market, as Brazilian local rates have declined by more than 100 basis points since their peak in early March. Companies have increasingly turned to the local market to raise debt, with debenture issuances tripling in recent years, often at variable rates. As such, the possibility of the BCB cutting rates by the end of the year would be crucial in lowering financing costs and improving cash generation for these firms. As a reference, some companies have seen their financing costs nearly double in 2022 due to the increase in Selic (+77% in 2022). On the other hand, a reduction in financing costs, could lead to increased consumption and investment, where durable goods, construction, and real estate sectors, would benefit from the beginning of a dovish cycle.

From the perspective of the stock market, although the initial reaction was positive since a proposal implying a greater deficit was expected, the following days have raised more doubts than answers as to how it will be financed and what other adjustments will have to be made to carry out the government's plan. In this sense, companies that have a significant percentage of their value associated with state benefits or subsidies, or companies that benefit greatly from certain types of exemptions, have fallen sharply, incorporating these risks. Some retail and industrial companies, among others, were particularly affected. We believe that if the government manages to deliver a clear formula for fiscal control, there will be room for rate cuts, and high-quality companies that benefit from this scenario will be interesting opportunities (rental cars, basic consumption, among others).

Kind regards, LarrainVial Asset Management Team.

LarrainVial S.A. LarrainVial Chile. Isidora Goyenechea 2800, 15th Floor, Las Condes, Santiago, Chile.

Tel.: +562 2339 8500Teléfono: +562 2339 8500

All Rights Reserved ©Copyright 2024

Chile

Chile Peru

Peru Colombia

Colombia English

English